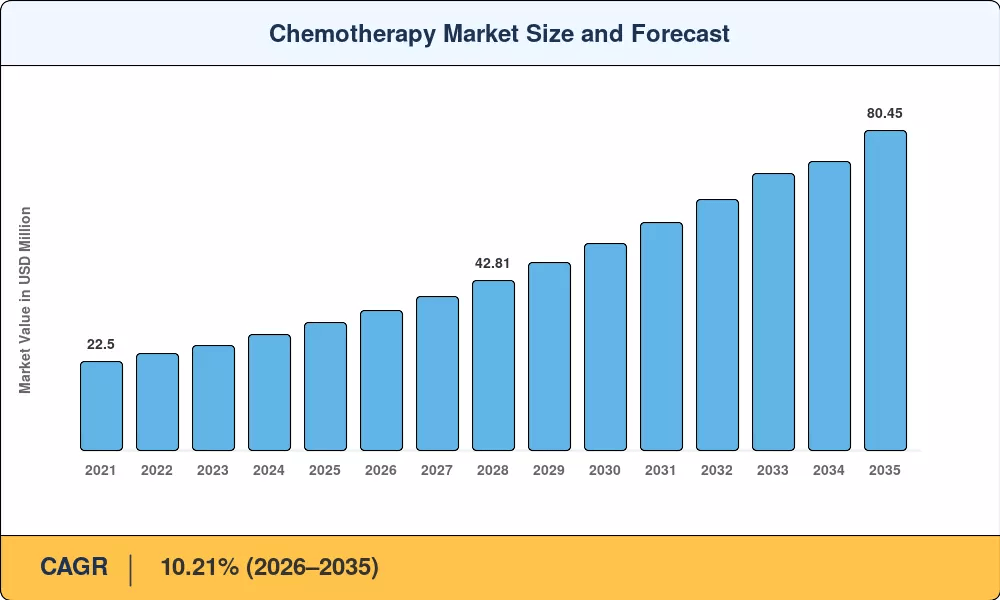

Chemotherapy Market to Surge from USD 35.24 Billion in 2026 to USD 80.45 Billion by 2035— Powered by Rising Cancer Incidence, Biosimilar Cost Reductions

NY, CA, UNITED STATES, June 11, 2026 /EINPresswire.com/ — As per Market Research Future, the global Chemotherapy Market size to reach USD 80.45 Billion by 2035 from USD 35.24 Billion in 2026, at a CAGR of 10.21% during the forecast period 2026–2035. The market base was estimated at USD 32.18 Billion in 2025.

The 10.21% CAGR—nearly double the growth rate of the broader pharmaceutical sector—is driven by three converging structural forces: the persistent rise in global cancer incidence (WHO estimates 20 million new cases annually by 2025), the regulatory acceleration of biosimilar and generic adoption cutting treatment costs by 30–45%, and the emergence of oral cytotoxic formulations that shift hospital-based oncology drug infusion toward at-home patient management.

National governments and healthcare systems are amplifying this momentum. The EU Beating Cancer Plan has committed EUR 4 billion to oncology infrastructure and access programs. India’s Ayushman Bharat (PM-JAY) health insurance framework and National Program for Prevention and Control of Non-Communicable Diseases (NP-NCD) provide dedicated grants up to INR 120 crore for State Cancer Institutes alongside launching widespread Day Care Cancer Centers in district hospitals.

China’s Healthy China 2030 initiative added 22 antineoplastic treatment regimen entries to the National Reimbursement Drug List between 2022 and 2024. Brazil’s Unified Health System (SUS) mandated that all SUS-accredited oncology centers stock a minimum formulary of eight platinum-based cancer drugs. Together, these initiatives are creating the population-scale treatment infrastructure on which cytotoxic drug therapy and antineoplastic treatment regimens depend.

Request A Free Sample: https://www.marketresearchfuture.com/sample_request/5791

Key Market Trends & Growth Drivers

Rising Global Cancer Incidence

GLOBOCAN 2024 data project 35 million new cancer diagnoses yearly by 2050, up from 20 million in 2022, with the highest incidence gains in low- and middle-income countries. This epidemiological fact underpins long-range demand for cytotoxic drug therapy as targeted and immuno-oncology drugs evolve. First-line and salvage chemotherapy continue to be important for around 60% of solid-tumor patients who are not responsive to precision therapies alone, ensuring the Chemotherapy Market remains a foundational pillar of oncology care.

Biosimilar Adoption Cutting Treatment Costs

Europe’s centralized and regional tender systems for traditional platinum-based cancer therapies—including cisplatin, carboplatin, and oxaliplatin—have dramatically lowered per-cycle infusion costs due to intense generic competition. Because these platinum compounds are small-molecule agents rather than complex biologics, market expansion relies on classic generic accessibility rather than biosimilars (which are strictly reserved for complex oncology monoclonal antibodies like trastuzumab and bevacizumab). The resulting drop in pricing has structurally expanded therapeutic volumes, enabling an increasing number of public hospitals across Southern and Eastern Europe to integrate standard intravenous chemotherapy protocols into local regional formularies.

Between 2022 and 2024 alone, the FDA authorized 14 combination chemotherapy indications and biosimilar versions of platinum-based cancer medications in European tenders, reducing treatment costs by 30–45%.

Oral Formulation Growth and Home-Based Cytotoxic Therapy

Evolving regulatory pathways and joint agency frameworks, such as the active initiatives led by the FDA and the Center for Research on Complex Generics (CRCG) concerning alternative bioequivalence modeling, continue to accelerate the translation of injectable chemotherapies into robust oral options. Oral antineoplastics—predominantly driven by staples like capecitabine, temozolomide, and lenalidomide—already account for a commanding 54.3% share of the Chemotherapy Market by route of administration.

The pipeline development of newer oral prodrug formats (such as oral taxanes) is intentionally designed to shift the balance of care away from highly resource-intensive, hospital-based oncology infusion suites to home-based management, aligning with post-pandemic patient preferences for at-home cytotoxic drug therapy.

Market Segment Insights

BY DRUG CLASS

Alkylating Agents: Dominant segment with ~40.8% share in 2025. Cyclophosphamide, ifosfamide, and temozolomide remain first-line choices in treatment guidelines for glioblastoma, non-Hodgkin lymphoma, and ovarian cancer. Their patent-expired status keeps unit costs low, ensuring high procurement volumes across both developed and emerging oncology drug infusion settings.

Antimetabolites: Fastest-growing drug class at 10.75% CAGR (2026–2035). Reflecting expanded use of capecitabine and pemetrexed in oral cytotoxic drug therapy schedules, allowing at-home administration and reducing hospital burden.

Plant Alkaloids (Mitotic Inhibitors): USD 5.12 Billion revenue in 2025. Taxane use in neoadjuvant oncology drug infusion protocols drives demand.

Antitumor Antibiotics: 9.85% CAGR (2026–2035). Doxorubicin and bleomycin demand in hematologic cancers fuels growth.

Other Drug Classes (Topoisomerase Inhibitors, Platinum-Based Agents): USD 2.88 Billion in 2025. Etoposide, irinotecan, cisplatin, carboplatin, and oxaliplatin remain backbone agents in combination regimens.

BY ROUTE OF ADMINISTRATION

Oral: Dominant route with ~54.3% share in 2025. Patient-preference data increasingly favor at-home dosing over hospital-based oncology drug infusion. Eliminates chair-time constraints, reduces nursing overhead, and aligns with post-pandemic care preferences.

Intravenous: Fastest-growing route at 10.85% CAGR (2026–2035). Underpinned by new platinum-based cancer drugs and antibody–drug conjugate (ADC) approvals that require hospital-based oncology drug infusion. Next-generation platinum agents with superior pharmacokinetic profiles drive volume expansion.

Other Routes (Intrathecal, Intravesical, Subcutaneous, Intramuscular): USD 1.15 Billion in 2025. Specialized oncology drug infusion for CNS and bladder cancers.

BY INDICATION

Lung Cancer: Dominant application with ~27.8% share in 2025. First-line platinum-based cancer drugs in non-small cell lung cancer (NSCLC) remain the standard of care even in the immunotherapy era, reflecting the global disease burden.

Blood Cancers (Leukemia, Lymphoma): USD 8.05 Billion in 2025. Multi-agent intravenous chemo protocols for acute leukemias and lymphomas drive sustained demand.

Breast Cancer: Fastest-growing indication at 10.95% CAGR. Landmark trial data supporting dose-dense antineoplastic treatment regimens and oral cytotoxic drug therapy in HR-positive settings propel expansion.

Other Indications (Colorectal, Ovarian, Gastric, Prostate, Stomach): USD 6.42 Billion in 2025. Combination cytotoxic drug therapy with targeted agents broadens the addressable patient pool.

BY END USER

Hospitals & Clinics: Largest segment, reflecting the capital intensity and regulatory requirements of hospital-based oncology drug infusion. Academic medical centers and comprehensive cancer centers operate the highest-volume intravenous chemo protocols.

Specialty Centers: Fastest-growing end user, reflecting the shift toward dedicated oncology infusion centers and community-based cancer care. Medicare policy changes and payer reimbursement evolution support freestanding infusion facility expansion.

Ask for Customization: https://www.marketresearchfuture.com/ask_for_customize/5791

Regional Outlook

North America — Dominant Market (~41.2% Share, 2025)

The United States generates approximately 82.5% of North American Chemotherapy Market revenue, driven by the 340B Drug Pricing Program enabling safety-net hospitals to procure antineoplastic treatment regimens at discounted rates, Medicare Part B oncology drug infusion reimbursement, and CMS reimbursement updates in 2024 that raised the average payment for cytotoxic drug therapy administration by 3.2%.

Canada is growing at 10.85% CAGR on Pan-Canadian Oncology Drug Review expansions. Mexico’s Seguro Popular cancer-coverage reforms contribute USD 0.89 Billion (2025), growing steadily on public-sector oncology investment.

Europe — Second Largest (26.8% Share, 2025)

Europe’s Chemotherapy Market benefits from standardized EMA approval pathways, biosimilar acceptance, and centralized procurement systems. Germany leads regionally with 23.4% of European share, as its statutory health insurance system covers virtually all approved cytotoxic drug therapy agents.

The UK is growing at 10.48% CAGR anchored by the NHS Long Term Plan cancer funding and the Cancer Drugs Fund, which allocated GBP 1.4 billion in 2024 for accelerated access to novel antineoplastic treatment regimens. France’s INCa-guided standardization contributes USD 1.72 Billion (2025). Italy’s AIFA biosimilar incentive policies and Spain’s regional health-system oncology expansion further underpin European market depth. The EU Beating Cancer Plan’s EUR 4 billion commitment provides a direct revenue catalyst across the region.

Asia-Pacific — Fastest-Growing Region (11.14% CAGR, 2026–2035)

Asia-Pacific is the highest-growth corridor in the Chemotherapy Market. China commands 38.6% of regional share, with the National Reimbursement Drug List adding 22 antineoplastic treatment regimen entries between 2022 and 2024 under the Healthy China 2030 initiative. India is growing at 11.65% CAGR on the back of Ayushman Bharat cancer-center expansion and the Tertiary Care Cancer Facilities Scheme, which provides grants up to INR 120 crore for State Cancer Institutes.

India’s bulk API manufacturing capacity—covering over 40% of global cytotoxic active ingredients—positions the country as both a consumption and supply hub. Japan contributes USD 2.45 Billion (2025) through NHI formulary coverage of intravenous chemo protocols. South Korea’s HIRA reimbursement reforms and ASEAN’s WHO-prequalified platinum-based cancer drugs adoption are growing at 10.92% and 12.05% CAGR respectively.

Middle East & Africa — Emerging Opportunity (9.85% CAGR, 2026–2035)

Saudi Arabia’s Vision 2030 health-sector investments include USD 3.2 billion earmarked for comprehensive cancer centers, each designed to deliver full-spectrum antineoplastic treatment regimens including intravenous chemo protocols and oral cytotoxic drug therapy. The UAE leverages medical-tourism oncology drug infusion demand, growing at 10.55% CAGR. South Africa’s NHI pilot oncology coverage contributes USD 0.32 Billion (2025).

Egypt’s 100 Million Healthy Lives cancer screening infrastructure is being repurposed for early cancer detection, funneling newly diagnosed patients into the Chemotherapy Market at earlier, more treatable stages at 11.25% CAGR. NGO and WHO cytotoxic drug therapy donation programs support access across Sub-Saharan Africa.

South America — Growing Presence (USD 2.58 Billion, 2025)

Brazil anchors South America’s Chemotherapy Market at ~58.3% of regional revenue, with the Unified Health System (SUS) as the largest single purchaser of chemotherapy agents in the region. A 2024 federal decree mandated that all SUS-accredited oncology centers stock a minimum formulary of eight platinum-based cancer drugs, driving procurement volume growth.

Argentina’s public-hospital antineoplastic treatment regimen expansion is growing at 10.42% CAGR. PAHO-supported cytotoxic drug therapy access programs and IDB-funded health infrastructure loans underpin regional market development.

Competitive Landscape and Recent Developments

The Chemotherapy Market exhibits medium concentration, with an estimated HHI below 1,200 and the top five companies holding a combined 35–42% revenue share. Competition centers on branded-generic portfolios, biosimilar launches, and novel fixed-dose antineoplastic treatment regimens. Large multinationals compete on pipeline depth and global distribution, while specialized generics manufacturers—particularly from India and China—compete on cost and API-supply integration.

The competitive landscape is stratified between large-platform innovators controlling end-to-end oncology drug infusion and ADC pipelines, mid-sized specialty firms focused on specific cytotoxic drug classes, and emerging-market generics manufacturers reshaping cost economics through API backward integration.

Read Detailed Insights: https://www.marketresearchfuture.com/reports/chemotherapy-market-5791

KEY COMPANIES AND RECENT MILESTONES

Hoffmann-La Roche (Roche): Estimated revenue share ~8–11%. Broad oncology drug infusion portfolio with Xeloda (capecitabine) and ADC pipeline including Avastin biosimilar combinations. Strategic positioning bridges targeted therapy and cytotoxic drug therapy.

Pfizer Inc. (2026): Announced a major oncology collaboration with Innovent Biologics valued at up to USD 10.5 billion to jointly develop 12 early-stage cancer therapies including antibody-drug conjugates (ADCs) and multispecific antibodies, strengthening its chemotherapy and oncology pipeline. Estimated revenue share: ~6–9%.

Bristol-Myers Squibb: Estimated revenue share ~5–8%. Diversified portfolio including Abraxane (nab-paclitaxel) and platinum-based cancer drugs, with strong combination antineoplastic treatment regimen integration.

Novartis AG (2026): Reported promising early-stage results for its experimental actinium-based radiopharmaceutical therapy for prostate cancer, showing strong anti-tumor activity even in patients previously treated with chemotherapy, further expanding its oncology and radioligand therapy portfolio. Estimated revenue share: ~5–7%.

Teva Pharmaceutical: Estimated revenue share ~5–7%. Cost-leader in off-patent chemotherapy generics, including generic alkylating agents and oral antimetabolites.

Eli Lilly & Co.: Estimated revenue share ~4–6%. Antimetabolite franchise with Alimta (pemetrexed) and Verzenio combination protocols, maintaining strong U.S. market presence.

Cipla Ltd. / Sun Pharmaceutical: Estimated combined revenue share ~6–10%. Leading emerging-market distribution for oncology drug infusion agents, with India-based API backward integration and Asia-Pacific and African market penetration.

Fresenius Kabi: Estimated revenue share ~2–4%. Hospital-pharmacy supply-chain integration for intravenous chemo protocols, with ready-to-use cytotoxic infusions and IV-oncology solutions.

Future Outlook: 2026—2035

By 2030, AI-driven precision dosing systems are expected to become standard within oncology care workflows, providing pharmacogenomic data integration and predictive machine learning models that anticipate individual pharmacokinetic variability to avoid severe dose-limiting toxicities. Platforms like Tempus integrated inside Flatiron Health’s OncoEMR span over 800 community-based clinical cancer locations, allowing thousands of providers to utilize multimodal data, track molecular profiles, and reduce the clinical friction that leads to severe adverse events.

Oral chemotherapy is projected to become the default first-line modality for an expanding set of indications, representing a fundamental evolution in patient care workflows. This market transformation places massive operational emphasis on specialized distribution pipelines, digital symptom trackers, and remote patient monitoring software designed to maintain high adherence and track side effects without relying on direct hospital visits.

Supply-chain regionalization and API sovereignty initiatives are accelerating. Post-pandemic supply-chain stress has prompted the U.S., EU, and Japan to pursue domestic API manufacturing for critical platinum-based cancer drugs. CHIPS-and-Science-style incentives being drafted for pharmaceutical ingredients could redirect USD 5–8 billion in capital expenditure toward reshoring cytotoxic API production, stabilizing supply and reducing shortage risk for the Chemotherapy Market.

The next decade will see market consolidation around antibody-drug conjugate (ADC) hybrid regimens that bridge targeted biology with classic cellular destruction. Driven by blockbusters like Enhertu and Kadcyla, the global ADC sector was valued at USD 18.60 billion in 2025 and is expected to climb past USD 34.80 billion by the mid-2030s.

ESG reporting mandates under the EU Corporate Sustainability Reporting Directive (CSRD) will require life science organizations to track supply chain footprints, adding a green-chemistry dimension to cytotoxic manufacturing as CDMOs phase out toxic solvents and maximize atom economy. Together, these forces underscore that patient access, cost efficiency, and commercial expansion are now aligned drivers propelling the Chemotherapy Market to its USD 80.45 Billion 2035 destination.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/oncology-drugs-market-12355

https://www.marketresearchfuture.com/reports/cancer-immunotherapy-market-592

https://www.marketresearchfuture.com/reports/targeted-cancer-therapies-market-27895

https://www.marketresearchfuture.com/reports/precision-medicine-market-925

https://www.marketresearchfuture.com/reports/biosimilars-market-1329

https://www.marketresearchfuture.com/reports/monoclonal-antibody-therapy-market-2089

https://www.marketresearchfuture.com/reports/oncology-biosimilars-market-21979

https://www.marketresearchfuture.com/reports/cancer-diagnostics-market-1962

https://www.marketresearchfuture.com/reports/radiotherapy-market-1526

https://www.marketresearchfuture.com/reports/cancer-vaccine-market-9087

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery